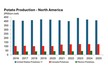

The 2023/24 potato crop increased 10 percent from the previous season, the largest year-over-year increase in the 13-NASS surveyed States since 1996. Following fall harvest, potatoes are stored to meet fresh-market and processor needs throughout the marketing year. Stocks also include potato seed to plant the following year's crop. On June 1, 2024, U.S. potato stocks totaled 66.8 million hundredweight (cwt)—up 19 percent from the 3-year average June stock volume (figure 5). June 2024 stocks represented 15 percent of the estimated crop, compared with 14 percent a year earlier.

More than 60 percent of the U.S. potato crop is destined for the processing market each season. Given the larger stock volume at this time of the marketing year, frozen and dehydrated processors are expected to use some of the 2023/24 crop into the early part of the 2024/25 marketing year (MY). An estimated 194.6 million cwt of potatoes was used for processing by the eight reporting States in 2023/24 through May 31 (table A1). Season-to-date volume of potatoes processed into dehydrated products (except starch and flour) total 33.6 million cwt—the highest in 3 years. Potatoes used for dehydrated products represented 17 percent of total processed volume, which is equal to the previous 3-year average for this period.

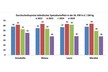

USDA, NASS reports monthly grower prices for fresh potatoes in 2023/24 have remained low, ranging from $10.20 to $10.60 per cwt between January and May (figure 6). In the 2022/23 MY, fresh potato prices ranged from $21.20 to $23 per cwt during the same period.

With ample supplies available, fresh potato retail prices, reflected by Bureau of Labor Statistics (BLS) Consumer Price Index (CPI), also fell in early 2023/24 MY, but have remained relatively flat since January 2024. If fresh grower and retail prices follow previous marketing year patterns, prices in July and August would be slightly above averages observed in January–May 2024.

Click here to read the full report.

Source: ers.usda.gov