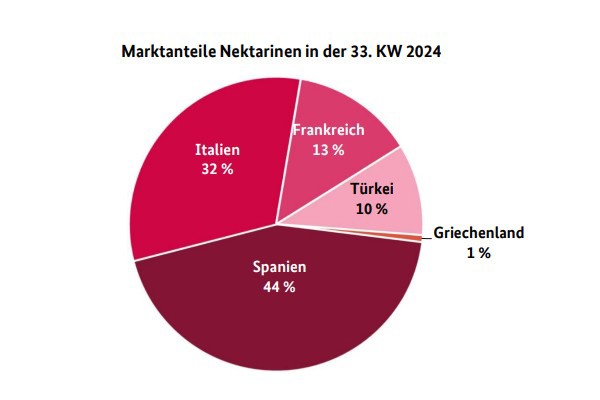

The stone fruit campaign entered its home straight: Deliveries of nectarines and peaches from Spain and Italy appeared to have decreased. Overall, Spanish and Italian producers recorded a better harvest than in the last 5 years. On the wholesale markets, Turkish, Greek and French shipments supplemented the situation with ever decreasing quantities. In general, interest was satisfied without major efforts. Due to the holidays, interest was not particularly strong in some cases. According to the BLE, the products occasionally left something to be desired in terms of organoleptic properties: Reduced shelf life and flavour weaknesses slowed down processing considerably and sometimes resulted in freely negotiable prices.

© BLE

© BLE

On the other hand, however, there were also some very appealing items on offer, which steadily increased in price. In Munich, the presence of Turkish imports expanded; with this measure, the distributors plugged the supply gap created by the limited Spanish and Italian deliveries. The fruit from Turkey and France was convincing in Berlin in terms of quality and calibre size, so that it could be accommodated relatively quickly. There were also some domestic items in the capital, but they were not very popular in calibre B at €6 per 4 kg carton.

Apples

The campaign continued and a certain change could be seen in the assortment: The presence of early varieties dwindled, while the importance of later varieties grew. Elstar, Boskoop and Tenroy were now available in larger quantities. Santana was a new addition to the product range.

Pears

Italian varieties dominated the scene in the form of Santa Maria and Carmen; Williams Christ and Abate Fetel had a complementary character. Turkish Santa Marie played a very important role. The already established domestic Clapps Liebling were now increasingly flanked by Williams Christ. The first German Conference also appeared sporadically.

Grapes

Italian batches predominated. In addition to many other varieties, Victoria, Michele Palieri and Black Magic were the most popular. Turkish Sultana gained market share and cost €12.50 per 5kg carton in Hamburg and between €2.75 and €3.00 per kg in Berlin. Spanish batches completed the range with small quantities.

Strawberries

Although the availability of domestic produce slowly declined here and there, considerable quantities of late varieties continued to flow onto the markets locally. On the demand side, a certain degree of customer saturation had set in: Sales options were becoming noticeably limited.

Apricots

The season was on the home straight: Deliveries dropped off noticeably. Some traders had already left the shops, and Italian and Spanish fruit in particular was no longer consistently available. The quality increasingly left something to be desired.

Plums

The arrival of the first domestic Presenta and Ortenauer plums heralded the last third of the season: Hanita were increasingly replaced and Cacak's Schöne also lost market share. In addition to some top varieties, Auerbacher, Bühler Frühzwetschge and Fellenberg were available from Germany as well.

Lemons

The Spanish Verna season was coming to an end: its presence was obviously diminishing. In contrast, South African Eureka gained in importance. Customers often had to dig a little deeper into their pockets for the latter.

Bananas

The holidays resulted in very limited demand on some markets. Although traders responded by reducing the supply, some of them had to lower their prices over the course of the week if they wanted to avoid surpluses.

Cauliflowers

Domestic supplies dominated and were monopolised at certain points. There were also Polish and Dutch batches in Berlin and Belgian batches in Cologne. Demand was not particularly strong and could be satisfied without difficulty. Nevertheless, prices often trended upwards, sometimes quite strongly.

Lettuce

Domestic batches predominated, with Belgian and Dutch shipments supplementing lettuce and Dutch and Spanish supplies of iceberg lettuce. The supply had expanded. Interest could not always keep pace with this. Overall, storage space was quite limited due to the holidays.

Cucumbers

The assortment consisted of domestic, Dutch and Belgian consignments. Although demand was not particularly strong, prices nevertheless rose: The price increases were partly due to a higher demand, but also to supply factors.

Tomatoes

The market was dominated by Dutch and Belgian goods. Italian and domestic lots only made a supplementary appearance. A fairly extensive offer met with restrained interest. Prices therefore often shifted downward.

Sweet peppers

Dutch deliveries characterised the market, while Turkish, Belgian and domestic deliveries complemented it. Availability was easily sufficient to cover demand. Demand was not particularly strong. In terms of price, Dutch and Belgian products mostly saw an upward trend.

Source: BLE