The International Air Transport Association (IATA) released data for global air freight markets showing that 2022 full-year demand for air cargo took a significant step back from 2021 levels but was close to 2019 performance.

Global full-year demand in 2022, measured in cargo tonne-kilometers (CTKs*), was down 8.0% compared to 2021 (-8.2% for international operations). Compared to 2019, it was down 1.6% (both global and international).

Capacity in 2022, measured in available cargo tonne-kilometers (ACTKs), was 3.0% above 2021 (+4.5% for international operations). Compared to 2019 (pre-COVID) levels, capacity declined by 8.2% (-9.0% for international operations).

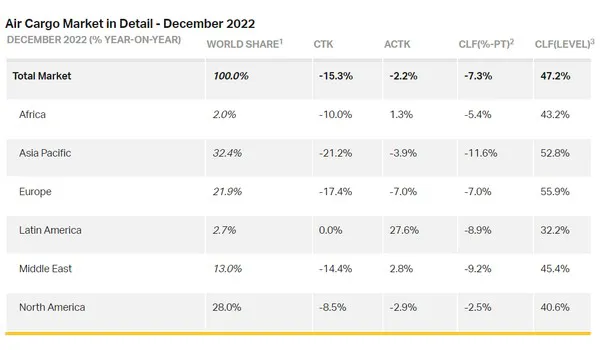

December saw a softening in performance: global demand was 15.3% below 2021 levels (-15.8% for international operations). Monthly cargo demand tracked below 2021 levels from March 2022. Global capacity was 2.2% below 2021 levels (‑0.5% for international operations). This was the tenth consecutive monthly contraction compared to 2021 performance.

2022 ended with mixed signals:

- Global new export orders, a leading indicator of cargo demand, have stayed at the same level since October. For major economies, new export orders are shrinking except in Germany, the US, and Japan, where they grew.

- Global goods trade decreased by 1.5% in November, down from a 3.4% increase in October.

- The Consumer Price Index for G7 countries indicated inflation tracking at 6.8% for December. The 0.6 percentage point drop compared to November (7.4%) was the largest over the course of year. Inflation in producer (input) prices reduced to 12.7% in October, its lowest level so far in 2022.

“In the face of significant political and economic uncertainties, air cargo performance declined compared to the extraordinary levels of 2021. That brought air cargo demand to1.6% below 2019 (pre-pandemic) levels. The continuing measures by key governments to fight inflation by cooling economies are expected to result in a further decline in cargo volumes in 2023 to -5.6% compared to 2019. It will, however, take time for these measures to bite into cargo rates. So, the good news for air cargo is that average yields and total revenue for 2023 should remain well above what they were pre-pandemic. That should provide some respite in what is likely to be a challenging trading environment in the year ahead,” said Willie Walsh, IATA’s Director General.

For more information:

Corporate Communications

Tel: +41 22 770 2967

[email protected]