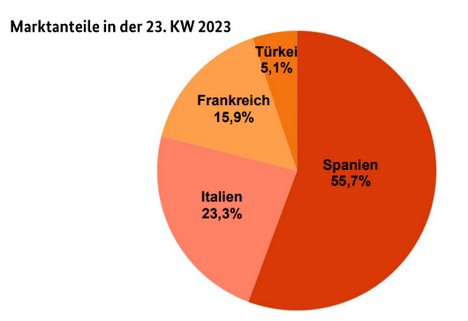

Spanish apricots dominated and were most likely flanked by Italians. Unloadings from France complemented. From Turkey came, on the one hand Matador; on the other hand the first sugar apricots also arrived, which cost € 25 per 10 kg in Hamburg and € 4 per kg in Berlin. Overall, availability had expanded; it was easily sufficient to meet demand. Demand was quite friendly, and customers were happy to help themselves. Particularly colorful and very appealing offers were quickly accommodated. Sometimes a wide price range was established on the markets, caused by diverging quality and non-uniform grades. As a result of the increased deliveries, the prices of the Italian and Spanish batches also trended downwards.

© BLE

© BLE

Click here for the full market and price report.

Apples

Customer interest slowly but surely shifted from alternative European produce to overseas imports. Although the domestic lots still held the top position in terms of volume, their presence melted away unmistakably. Italian and French products also appeared to be losing ground.

Pears

South African shipments dominated; Chilean and Argentinean followed. Fruits from the Netherlands, Belgium, Italy and Turkey did not go beyond a supplementary status. In Berlin, the first European summer pears appeared toward the weekend with Spanish Castell.

Table grapes

Chilean and South African imports weakened in unison, with Italian and Egyptian lots arriving in greater numbers instead. On the whole, interest was satisfied without major efforts. On occasion, accommodations had improved as a result of the summer weather.

Strawberries

Availability had expanded noticeably as a result of the summer weather. Local fruits apparently predominated. They were flanked by Dutch batches. In Berlin and Hamburg, there were also very attractive Polish shipments, which met with a friendly reception.

Peaches and nectarines

Spanish inflows dominated; their presence had again increased. Italian inflows followed in terms of importance. A few Turkish and Greek shipments were merely of a supplementary nature. French batches were only to be found in Cologne. In general, interest was not particularly strong.

Cherries

Spanish deliveries formed the basis of the assortment. Turkish fruits gained noticeably in importance: Napoleon and Sahili were increasingly in demand. Pella came from Greece. Italy supplied Ferrovia, which was convincing in terms of taste and firmness.

Lemons

Spanish deliveries outweighed South African ones. Italian and Greek supplies were at most of a supplementary nature, and Turkish imports disappeared completely from the range. Demand was met without difficulty.

Bananas

Supply and demand were sufficiently balanced. As a result, traders rarely had cause to modify their previous demands. On several occasions, they adjusted their calls downward to improve accommodation.

Cauliflower

Most of the business was with German products; unloadings from Italy, Belgium, and the Netherlands were very rare. On several occasions, domestic items were available without competition.

Salads

German offers predominated. In the area of colorful lettuces, endives and lettuces, they were flanked by Belgian articles. In the iceberg lettuce segment, there were Dutch and a few Spanish deliveries in addition to the domestic batches.

Cucumbers

Domestic, Belgian and Dutch batches shared the market action among themselves for snake cucumbers. Availability grew and outstripped accommodation. Traders responded by lowering demands, which at least somewhat revived subsequent sales.

Tomatoes

Dutch and Belgian deliveries apparently predominated. Italy participated in the marketing only with cherry tomatoes, which selectively left the trade in the course of the week. Local fruits were at the top of the price list, but could still be accommodated in a friendly manner.

Sweet peppers

Dutch, Belgian and Turkish deliveries formed the basis of the range. The imports were flanked by a few domestic lots, but these were by no means to be found at all markets. Business was generally fairly quiet.

Asparagus

Slowly, the campaign turned into the home stretch: The dominant domestic supplies were dwindling, and interest was no longer as strong. A certain degree of customer saturation could not be denied after Whitsun. However, availability limited so strongly in certain areas that retailers were able to increase their calls without any problems.

Source: BLE